Once your home is on the market and buyers have been to view, your Estate Agent will start to send through feedback from each applicant explaining exactly what they thought of your property. There are opportunities here to try and make sense of the comments that come back and possibly act upon them if no offers are forthcoming. Sometimes feedback can be very revealing and point to a specific problem that needs to be addressed or overcome.

If a buyer has one particular objection about a property then this is often a positive sign. So if they are worried about the busy road but like the property generally then it’s the job of your Estate Agent to sell them the positives and try to persuade them to make a compromise on this particular point, perhaps by mentioning that similar properties on a quieter road would cost that much more. Or maybe if the garden isn’t quite as big as they hoped, the generous living space will make up for this and again, the buyer may be prepared to compromise.

Of course if the buyer reels off a whole list of reasons why they’re not interested or says that they simply “didn’t get the right feel” then it’s unlikely that they’ll be making an offer. Similarly if the house itself is too small for their needs or the location just isn’t right, it’s unlikely things will progress.

On average you’ll probably need around 8-10 viewings to receive an offer. If you’ve had umpteen viewings with no offers and lots of negative feedback then this is the market’s way of telling you that the price is probably too high. Similarly, no viewings at all after several weeks usually either means the price is too high or that the property isn’t being marketed in the right way. Take a look at the photos your agent has produced. Are they crisp, well composed and brightly lit? If the photos are poor then buyers will assume the house is poor so don’t put up with poor quality marketing from your agent. Do you need a For Sale Board? If you haven’t had one up to this point, then it’s worth considering as it may attract fresh buyers.

Finally be prepared to act upon feedback and liaise closely with your Estate Agent throughout the process. If buyers keep pointing to that damp patch on the ceiling or that peeling paintwork on the front door, then you really need to get it sorted. Communication is key and if you listen to what the market is telling you then you’ll be well on the way to finding that right buyer and achieving a sale.

As the British and Coventry property market navigates the ongoing economic turmoil, many Coventry homeowners and landlords may feel uncertain about the future.

However, up-to-date data suggests that the 2023 property crash predicted by the many newspapers and the usual clickbait doom-mongers in the lead-up to Christmas on social media, may not be as bad as initially thought, and there are reasons to be cautiously optimistic.

According to property website Rightmove, the average asking price of a home for sale in the UK rose by just £14 in February.

While this might sound like cause for concern, asking prices remaining flat rather than falling could be seen as a positive sign for the year ahead. Remember that they are only what people are asking (and not necessarily achieving).

So, what exactly is happening in the Coventry property market?

Well, it all starts with realistic pricing.

Thankfully, most Coventry sellers are heeding their estate agents’ advice and being more realistic on price, helping maintain market stability.

If you are realistic with pricing, the property should sell.

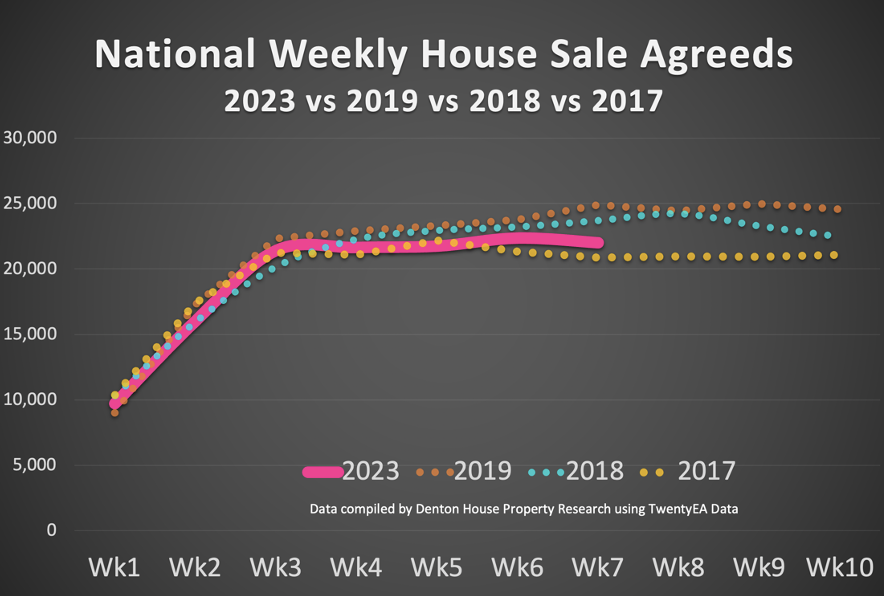

The time it takes to get a property to sale agreed upon has increased nationally from 21 days in the summer of 2022 to around 50 days in Q1 2023.

Additionally, despite the turbulent economic conditions, buyer demand is rising. Rightmove also reported in the national press that the number of people contacting estate agents has increased by 11% in the last two weeks compared to the same period in 2019.

The number of sales agreed upon has also rebounded.

Nationally, from 1st January to the 19th February 2023,

134,886 properties had been sold subject to contract in the UK.

Not a good figure when I compare it with the same year-to-date sale agreed figures from the last couple of years.

2022 – 173,607 properties sold stc

2021 – 193,607 properties sold stc

But the last couple of years have been extraordinary for the UK property market and should be taken with a pinch of salt in some respect. We must compare 2023 with more normal years, like 2017/18/19/20. This tells a different story.

2020 – 151,694 properties sold stc

2019 – 143,504 properties sold stc

2018 – 138,665 properties sold stc

2017 – 134,503 properties sold stc

In Coventry (CV6 to CV8), in the first seven weeks up to the 19th February 2022, 961 properties sold subject to contract.

This year, from the exact 1st January to the 19th February timeline, 740 properties have sold stc, which is lower, yet in the same ballpark as 2017, 2018 and 2019.

Yet it is all terrific selling a house (subject to contract); it is still only sold subject to contract, meaning the sale could fall through (as it is not legally binding).

As an agent who likes to delve deeper into statistics, I considered the ‘net property sales’. (Net Property Sales being the gross number of properties sold that week less the sale fall throughs in the same week).

In the three months leading up to the Mini-Budget in September 2022, there was an average of 17,801 ‘net property sales’ per week in the UK. That dropped by 34.7% two months after the Autumn Mini-Budget to an average of 11,624 ‘net property sales’ per week in the UK.

In the last five weeks, that has rebounded to 17,050

‘net property sales’ per week.

And when you consider the average for the same five weeks in 2017/18/19 was 18,330 ‘net property sales’ per week, we are close to what many considered a normal market.

Improving market conditions has been supported by a reduction in average mortgage rates. Homebuyers taking out a five-year fixed-rate mortgage with a 15% deposit can expect a rate of 4.39% (correct at the time of writing with HSBC), down from an average of 6.1% in early October. This reduction in mortgage rates may have contributed to the recent increase in buyer demand.

These positive signs in the market have led some experts to suggest that a ‘softer landing’ for the UK property market than initially expected could be on the horizon.

The combination of sellers being more realistic on price and an improving picture of the number of agreed-upon sales suggests a more positive outlook for the property market.

I advise Coventry homeowners coming to market in the upcoming spring season to use their agent’s expertise and get the price right the first time to find the right buyer more quickly. If you do wish to chance a higher asking price, only do so for no more than two weeks. If you haven’t sold by then, take the agent’s advice and realign your asking price.

562 Coventry homeowners have realigned their

asking prices since 1st January 2023.

While it’s true that some first-time buyers may still be priced out of their original plans and may need to look for a cheaper property, save a bigger deposit, or factor higher monthly mortgage repayments into their budgets, there is still cause for optimism.

There is still a considerable demand for buying property in Coventry – renting is becoming increasingly unattractive for many people as rents are increasing by double digits percentages.

It is important to remember that purchasing a property always involves a trade-off between what one desires and what is affordable, regardless of the market conditions. For example, while a four-bed detached house may be out of reach, a larger and older three-bed semi-detached property may be a more realistic option (and probably have similar square footage).

Coventry landlords looking to invest in buy-to-let homes – now may be a good time, as rising rents could offer attractive returns.

Of the 1,462 properties let in Coventry since the 1st January 2023, the average rent achieved has been £1,205 per month. This is a significant drop in the number of properties let in the same first seven weeks of the years of 2017/18/19 and a massive increase in rents.

Finally, the newspapers will be full of news about house price drops in the coming months. All the indexes report house sales where the sale agreed price was offered nine to eleven months ago and completed (i.e., monies and keys handed over) three or four months ago. This peculiar time lag means the house price data is nearly a year old before publication.

So, if you decide to buy a home on that information, you are using old property data. In late 2021/early 2022, there were 30+ viewings per property, and people paid way over the asking price to secure a property. Now there is more ‘normality’ in the Coventry housing market; today’s prices are also more normal (at or slightly below the realistic asking price). So yes, the house price indexes will show a reduction in house prices. The newspapers will say house prices are crashing, yet when it is explained I have above … whilst it is not a newspaper clickbait title – it is the truth and it’s more of a return to more ‘normal house prices’.

So, prepare for clickbait newspaper headlines of a house price crash (because ‘bad news sells newspapers’ as the saying goes).

Also, prepare for the doom-mongers to quote the bad news of the earnings-to-house prices ratio at one of its highest levels ever.

Earnings-to-house price ratios are a poor measurement of health in the UK property market. Instead, I believe Nationwide’s measure of first-time buyer mortgage payments as a percentage of take-home pay is better (as it is actual pound notes out of actual pay packets).

The Nationwide measure of first-time buyer mortgage payments as a percentage of take-home pay has grown for first-time buyers from 30.4% in Q4 2021 to 39.4% in Q4 2022 … a massive rise! Yet mortgage interest rates have dropped since then (so that percentage will fall). Also, to give some context, let us not forget that percentage in 1989 was 48.4%.

Ultimately, Coventry homeowners and landlords should decide, based on their unique circumstances, rather than being swayed by newspaper headlines or general market trends. Anyone uncertain about the property market’s future should contact me for my opinion, advice and guidance.

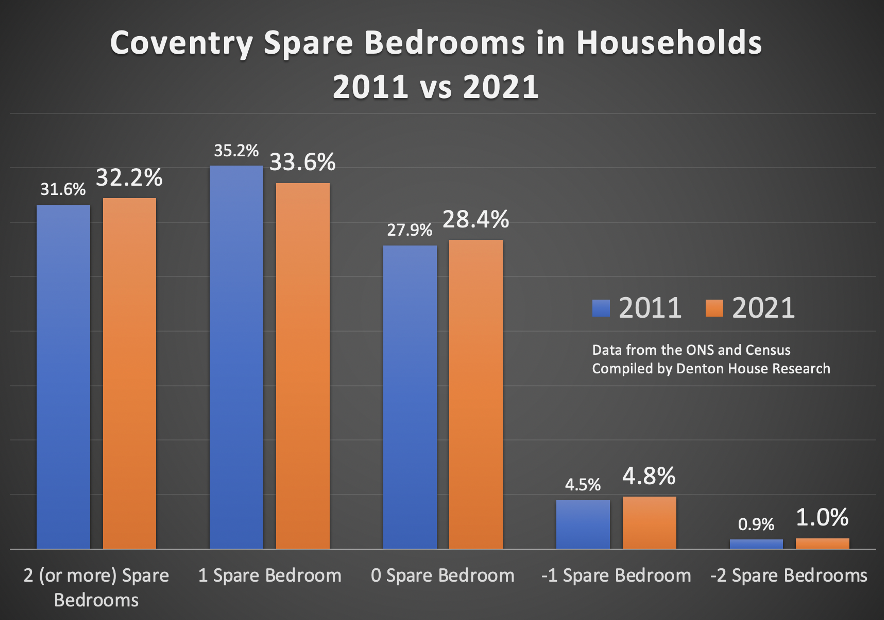

An additional 5,002 spare bedrooms have been locked out of the Coventry housing market since 2011 as Britain’s ageing population means the country’s stock of homes is being used more unproductively.

The number of spare bedrooms in Coventry between 2011 and 2021 increased from 126,483 to 131,485.

The number of Coventry households living in properties with at least two spare bedrooms (i.e., spare ‘spare’ bedrooms) increased by 2,575, from 40,626 households to 43,201 households between those ten years.

That means 32.2% of Coventry households

have two or more spare bedrooms.

And this isn’t just a local issue; Britain has 8,902,471 properties with a spare ‘spare’ bedroom (i.e., they have two or more spare bedrooms).

Before I dive deep into the issue of these ‘spare’ spare bedrooms, let me look at the ‘occupancy rating’ of all households in the country.

There are 8.26 million households with one spare bedroom, 6.57million households with no spare bedrooms (i.e., the household’s accommodation has an ideal number of bedrooms), 880,672 households where they are classed as over-crowded under the ‘Bedroom Standard’ by one bedroom and 173,751 households where they are classed as over-crowded under the ‘Bedroom Standard’ by two bedrooms.

The ‘Bedroom Standard’ allocates a separate bedroom to each of these groups (according the Office of National Statistics):

adult couple

any remaining adult (aged 21 years or over)

two adolescents (aged 10 to 20 years) of the same sex

one adolescent (aged 10 to 20 years) and one child (aged 9 years or under) of the same sex

two children (aged 9 years or under) regardless of sex

any remaining child (aged 9 years or under)

So, with this serious overcrowding, why is this under-occupation happening and is there a better use for these homes?

Britain has an ageing population. Just over 1 in 5 (18.6%) of Britain’s population are aged 65 years or older,

compared with 1 in 6 (16.4%) a decade ago.

In the last ten years, many of Britain’s baby boomer generation (currently aged 59 years to 77 years of age) have entered retirement. Most of these extra bedrooms are in homes owned by these baby boomers, who are probably still living in the original family homes they bought in the 1980s or 1990s to raise their children, yet still live there years after their children left home.

And it will get worse throughout the 2020s as the number of Brits living in homes greater than their needs will grow further as the demographics of the British population shift.

There are 68,247,855 bedrooms in England & Wales, and even if nobody shared a room, there would be enough for every one of the 59,597,542 of us to have a bedroom and still have 8,650,313 spare bedrooms! They are very unequally distributed between households.

What’s the answer?

Some on the left suggest we forcibly make these older mature Coventry homeowners people move to smaller homes. Yet, it’s their property; they paid the mortgage on it for years (especially when mortgage interest rates were 15% and above), and thus, it’s their choice if they want to move or not.

Some of the difficulties are that downsizing in Coventry often needs to make financial sense for mature homeowners.

Most mature Coventry homeowners live in average-priced homes and suitable bungalows, even though they are smaller, often cost as much, if not more, than their large family home.

This issue will slowly worsen in the coming twenty years, so what are the options?

There is a necessity to motivate builders to build suitable properties for these mature homeowners to move into and to change the dynamics of the available properties to buy. For example, there are only 2 million bungalows in the UK, and we only built just over 1,800 new bungalows in 2020, yet seven in ten UK people (c. 10.7 million) aged over 65 want to live in a bungalow.

Secondly, there needs to be reform of the taxation rules on housing. Taxation works on the carrot or stick method.

The ‘stick’ could make it less attractive to stay in larger houses by increasing the higher council tax rates in the higher council tax bands. The ‘carrot’ could incentivise mature homeowners to downsize with allowances on stamp duty or inheritance tax, thus making a move easier.

However, the cost-of-living crisis and heightened energy bills could be doing the Government’s job for them.

The number of larger Coventry homes owned by mature homeowners, often for 25 years plus, has been snowballing in the last six months.

This is good news for younger families that can afford to jump from their smaller homes, yet many can’t afford to make the jump for the same reasons why mature homeowners are moving home.

For example, of the 181,195 properties put on the market in the UK in November and December 2022, 56.9% were under £350,000. However, of the properties sold in the UK since Christmas 2022, 66.3% of them have been £350,000 or less.

This means those homeowners in the middle to upper levels of the Coventry property market need to be very realistic with this pricing as the supply of the mid/high range properties is outstripping the demand.

Whilst it is not a good distribution of housing if you have some people in overcrowded households and others with spare bedrooms, everyone should be able to choose how to live.

Many Coventry homeowners delay downsizing because they prefer to grow old in their family home rather than downsize. However, I often see mature homeowners downsizing too late when say, they have had a fall, are unable to manage the basics of gardening or cleaning, or the home becomes a physical hazard.

This downsizing phase will continue to grow, peaking in the mid-2030s.

The issue is, I cannot see builders or the Government building hundreds of thousands of bungalows in the next decade.

So maybe, you should consider making a move in the next few years, when you will have a better choice of bungalows to move to and you are able to put your stamp on it when you are in your 70’s and before you are unable to in your mid/late 80s?

If mature homeowners have large properties earned from working hard and paying taxes, then quite frankly, that is nobody else’s business and no one should force you out!! You might want that extra space for children and grandchildren to come and stay or as office space, a television room or a hobby room. Yet please, I must stress these are only suggestions.

Current market conditions for property sales are giving mixed signals. High demand from buyers but little to choose from is still providing upward pressure on prices. At the same time there is a reluctance amongst some sellers to ‘take the plunge’ and list their property for sale.

Q. But what is there to be afraid of?

Conversations with potential sellers show that there is a pattern here, generally the reluctance is due to fear of not being able to find a suitable onward property. The reason: there’s not much available at the moment!!

This catch 22 scenario is not uncommon in the housing market and is certainly not a new phenomenon, after all who wants to sell and then be left homeless or forced to go into rented.

In reality this ‘doomsday’ scenario’ is not a realistic pitfall. The advantage of the English & Welsh property market is the flexibility of the system. Until exchange of contracts there is no legal obligation to go through with the sale and no possibility of being forced to move. This ‘flexibility’ of course has plenty of downsides including gazumping (when another buying outbids the original buyer), gazundering (when a buyer reduces their offer at the last moment), withdrawal, fallthrough, etc.

In Scotland by contrast, once an offer is accepted, the buyer is contractually obliged to go through with the transaction, as is the seller. So one can understand a reluctance of Scottish sellers to go on sale if they haven’t found somewhere to go. But in England out system provides that flexibility and choice right to the finish line, meaning if a seller can’t find somewhere to move to then ultimately they don’t have to go through with the sale. So the reality is that there is no risk in going on sale.

Q. But isn’t it expensive to go on the market? We don’t want to waste money unnecessarily?

If you use a traditional estate agent there’s no cost either as fees are only charged upon completion of sale.

For further advice on selling or buying in this ever changing market speak to one of our property agents who will be delighted to help.

The Coventry housing market over the last three months is now becoming more ‘normal’ after the last couple of years of insane demand when the lockdowns started a race for space!

Even with the blackening economic doom-mongers forecasting a harsh slowdown in the British property market, the number of people buying and selling their homes is still very good for the time of year.

Whilst many homeowners are reducing their asking prices, it is not the 20% (some even said 30%) drop some property commentators and newspaper journalists had predicted.

Looking at the stats for Coventry for the last three months since the disastrous Truss mini budget – they make good reading.

Of the 978 Coventry properties that have sold (stc) since late September, the average length of time it took to achieve a sale was 36 days.

Interesting when you split it down by price, in Coventry:

Under £100k – 36 days

£100k to £200k – 29 days

£200k to £300k – 37 days

£300k to £400k – 49 days

£400k to £500k – 46 days

£500k to £1m – 41 days

£1m and above – 105 days

And by type:

Coventry Apartment/Flat – 40 days

Coventry Terraced/Townhouse – 35 days

Coventry Semi-Detached – 29 days

Coventry Detached – 43 days

The latest sold price data from the Land Registry shows that Coventry house prices currently remain 12.6% higher than they were 12 months ago; the rate of growth has dropped significantly.

Last month, Coventry house prices dropped by 0.3%; thus, we are seeing the first sign that the property market is starting to cool.

With interest rates at 3.5% and further increases likely in 2023, that will undoubtedly spur ongoing cooling in Coventry property values yet it’s doubtful we will see the Coventry property market go into the deep freeze that many doom-mongers were predicting.

As I said in recent articles on the Coventry property market, we will see a 5% to 10% reduction in Coventry house prices over the next 12 to 18 months.

That will only take us back to the prices achieved in mid/late 2021 or early 2022 (depending on the property type).

Landlords have experienced double-digit rent growth in the last 12/18 months with a shortage of rental properties coming onto the market. I cannot see this changing in the short term, so I expect rents to be a further 10% higher by Christmas 2023.

Last week I stated it is not always wise to only focus on house prices but also take reference from the number of property transactions completed that feed the fire of the British property market.

For example, in March 2021, 135,670 properties sold, yet a month later, it dropped to 87,600. A couple of months later, it rose again in June 2021 to 165,290 homes sold (for it to drop to 64,000 in July).

Whilst this is good news for estate agents and removals companies, it can skew the property market and put undue pressure on the property market (pressure which could cause a housing crash if not put under check).

Like most things – slow, steady and consistent is the preferred option for the property market. Throughout 2022, the number of properties selling in the UK has been a steady average of 68,832 per month, ranging from a low of 61,800 in January 2022 to 72,200 in July 2022.

This consistency will continue into 2023 and a return to a more ‘normal’ housing market.

One final thing I have noticed about the Coventry property market in the last six months is the number of larger properties coming onto the market that last sold over 25 years ago.

Homeowners in their 20s, 30s and early 40s tend to move every five or six years, yet when they reach their late 40s and 50s, they tend to stay put for longer. These properties only tend to come on the market when people pass away or must be sold for nursing home fees.

These mature homeowners are downsizing for several reasons. Their children have flown the nest and they’re rattling around in homes with accommodation they don’t need. Many are being driven to sell their large homes in light of mounting energy bills, high inflation and never-ending maintenance costs that larger properties demand.

The second reason is that the recent rises in Coventry house prices has meant the money released to downsize has grown, meaning if these mature homeowners sell up and cash in to more manageable properties, the amount of money released is quite impressive.

In conclusion, 2023 is going to be a more ‘normal’ year, akin to the 2016 to 2019 years. Coventry homeowners need to be realistic with their pricing, yet as over eight out of ten sellers buy another home, the one you buy will be lower.

If you are considering selling your Coventry home in 2023 and would like a chat about your options, feel free to drop me a line or call the office.

More Coventry homes are now coming up for sale. This is excellent news for Coventry homebuyers and Coventry landlords because as properties are no longer flying off the shelf as they did last year, the number of properties available to buy is beginning to return to long-term averages.

This means there is greater choice for Coventry buyers and this will reduce the pressure on Coventry house prices and return us to a more normal Coventry housing market for buyers (and sellers).

The average UK estate agency now has 25 homes for sale, the highest level of properties on the market since December 2021

(when it was 21 homes for sale).

However, properties per estate agency brand is not the best judge of the property market.

Let’s look at the actual Coventry stats, which tell a slightly different story.

Coventry Detached Homes – Dec 2021, 207 available and today, 319 available – an increase of 54%

Coventry Semi-Detached Homes – Dec 2021, 256 available and today, 514 available – an increase of 101%

Coventry Terraced/Town Houses – Dec 2021, 198 available and today, 386 available – an increase of 95%

Coventry Apartments – Dec 2021, 256 available and today, 259 available – an increase of 36%

Overall, an increase of 59% – year on year.

(The data for Coventry is calculated by looking at all properties and plots for sale within a 5-mile radius of the centre of Coventry).

This growth in properties for sale has been seen across all areas of the British Isles. This is important because when there is a more significant availability of homes for sale, this diminishes the increasing pressure on house prices.

So how does a low number of properties for sale make such a huge difference?

Coming into the early spring of 2022, the levels of properties for sale were low (as seen from the low December 2021 stats above). It was ‘Hobson’s choice’ for buyers, so they had to pay top dollar to secure their Coventry home.

The value of Coventry properties that had their sale agreed upon in the early spring of 2022 (and completed their sale in September 2022) are 15.3% higher than those Coventry properties that had a sale agreed upon in the spring of 2021.

The number of properties estate agents have to offer buyers is increasing; this will boost the choice for Coventry buyers, meaning we will move into a more balanced Coventry housing market.

Nevertheless, it’s vital that Coventry sellers place their properties, when they go onto the market, in line with what Coventry homebuyers are prepared to pay, given the current hit to their buying power initiated by higher interest rates.

Coventry house prices are not expected to crash in 2023,

yet they will be lower than in 2022.

If you are buying and selling in the same property market, it doesn’t matter what happens to property prices.

Also, some might say waiting for Coventry house prices to drop will enable them to grab a bargain.

Well, sorry to ‘rain on your parade’, but you should read my recent article that discusses what would happen if Coventry first-time buyers waited for Coventry house prices to drop. If they waited, because interest rates are rising, the extra mortgage payments would cost them a lot more than the savings made on the purchase price. (Send me a message if you want a copy of it).

What has an effect on the value of your Coventry home is the number of properties for sale at any one time compared to the number of buyers. When there is an over-supply of homes for sale, prices go down, and with reduced demand, house prices will go down. So how do the stock levels of properties for sale compare to the past?

If you recall at the start of the article, I stated the average UK estate agency had 25 properties on their books now. In 2018/9, that average was 36 properties for sale (and for added comparison, the long-term average, since records began in 2016, is 49 homes for sale).

As you can see, whilst stock levels have grown, we are a long way off the long-term average.

A great way to determine what will happen to the property market is by measuring that stock level (i.e., the number of properties for sale). Check once a month and see how many properties are for sale. Let me break that down for Coventry specifically and how you can judge the market from your sofa.

There are 1,572 properties and plots for sale in Coventry now. To give context, the long-term 16-year average is 2,200 properties and plots for sale, yet in the credit crunch of 2008, it reached 3,631 properties and plots for sale at one point.

I envisage some component of scarcity to persist in the Coventry property market, meaning whilst the house prices that were being achieved in the spring of 2022 won’t be replicated in 2023, it also won’t fall dramatically next year.

The incentives and impetuses to move home have changed in the last six months and will continue to do so into 2023.

As I have written before, there are a larger number of mature homeowners in their 60s and 70s downsizing to help with heating bills, whilst the desire for more space means younger families will continue to look for new homes to live in, in 2023.

If younger 20-somethings can access the Bank of Mum and Dad for mortgage deposits, they will also carry on buying. This is especially true because double-digit rental inflation makes renting quite expensive compared to buying (even with the increased interest rates).

These are my thoughts on the Coventry property market this week. Do put in the comments (or send me a message) your thoughts on the matter discussed and any other property-related topic you want some advice and opinion on.

For tenants, especially over the last 12 months, it has become progressively more challenging to find a Coventry rental home, thus making the rent they must pay go up. This state of affairs in the property market isn’t showing an indication of getting any easier either, making for a hard time for Coventry renters.

So, what is the reason behind the Coventry rental property shortage, and what does this mean for existing Coventry landlords or those potential investors considering buying a Coventry buy-to-let property soon?

Several different components are making the perfect storm in the UK property market.

Firstly, the number of households in the UK.

The UK has not been building enough homes for the last 20 years. I appreciate that parts of Coventry seem like one huge building site, yet as a country, we are woefully undersupplied with property to live in. This has meant house prices continue to rise due to demand.

The government have known about this issue for decades. The Barker Review of Housing Supply published in 2004 stated that the UK had experienced a long-term upward trend of 2.4% in real house prices since the mid-1970s because of a lack of house building. The report stated that 240,000 houses needed to be built each year to keep up with demand.

The average number of houses built since the mid-1970s has been around

165,000 per year, meaning the UK is short of 3,375,000 houses

(i.e. 45 years multiplied by 75,000 missing homes per year).

Several years ago, the government set a target to build 300,000 new homes each year to address this issue.

However, in 2019/20, the actual number of homes delivered stood at just 243,770. In 2020/21, the number of properties built dropped to only 216,000 new homes. In a nutshell, there are fewer available homes to buy, meaning fewer available homes to rent.

Secondly, Coventry tenants are staying in their rental homes longer.

A Coventry first-time buyer’s average house deposit is £37,159

(the UK average deposit is £53,935).

The average rent of a Coventry property in November 2022 is £1,091 per calendar month (up from £879 per calendar month in February 2020) – quite a rise!

These numbers translate into Coventry renters not being able to pay the rent and be able to save for a deposit, or if they are saving, it is taking a lot longer to save for a deposit due to the cost-of-living crisis and higher rent costs.

Also, many Coventry tenants have decided to stay in their existing rental homes because of the rent rises. Many landlords are less inclined to raise the rent on an existing property when they have a decent tenant who keeps the property in good condition and pays rent on time. Anecdotal evidence also suggests that rent arrears in those properties are dropping as tenants know if they don’t pay the rent, the chances are they will have trouble finding another property, and if they do, they will have to pay a lot for their next rental home.

For Coventry landlords, this is all positive news – tenants are staying for longer in their Coventry rental properties, arrears are lower, and void periods are less likely. When it comes to the market there is less competition (because of the decrease in the availability of Coventry rental properties) so this makes the investment an even better bet.

Thirdly, landlords are selling up on the back of recently increased house prices.

It would be difficult for Coventry buy-to-let landlords to ignore the rising property prices in recent years.

The average property value in Coventry in the summer of 2022

was 12.8% higher than in the summer of 2021.

For some Coventry buy-to-let landlords, especially those who were classified as ‘accidental landlords’ (an accidental landlord is a landlord who never chose to become a landlord, it was just after the Credit Crunch of 2008/9, they found themselves unable to sell their property, so they temporarily let their own property out), they chose to ‘cash in’ on the higher house prices. This would have also contributed to the lack of available Coventry homes for rent.

Yet everything isn’t all sweetness and light for Coventry landlords.

Landlords have a few costs to consider before investing in buy-to-let, including everything from regular refurbishment costs, buildings insurance, letting agents’ fees, income tax, and, not forgetting, stamp duty.

Talking of costs, one issue some Coventry landlords are facing is their failure to plan financially for the recent mortgage interest rate rises. Some Coventry landlords may have become complacent to the ultra-low Bank of England base rates we have had since 2008 and, therefore, may need to sell their rental property, which, if bought by a first-time buyer, will remove another property from the Private Rented Sector.

Another hurdle to jump is the proposed new regulations requiring better energy efficiency for rental properties. It is proposed all new tenancies must have at least a minimum of a ‘C’ rating for their EPC (Energy Performance Certificate) from 2025 (and 2028 for all existing tenancies).

Therefore, as a buy-to-let Coventry landlord, it is wise to do your research to make sure the buy-to-let opportunity is correct for your rental portfolio, particularly when it comes to weathering any impending financial storms.

Landlords need to consider the returns from their

Coventry buy-to-let investments.

Landlords can earn money from their buy-to-let investments in two ways. One is the property’s capital growth, and the other is the rental return (often expressed as a yield). In 96% of buy-to-let investments, there is an inverse relationship between capital growth and yield (i.e. properties that tend to go up in value quicker will have lower yields 96% of the time – and vice versa).

Getting the best balance of yield and capital growth depends on your current and future needs from your Coventry buy-to-let investment.

If you would like me to review your portfolio and ascertain if your existing portfolio will match your current and future needs for the investment – whether you are a client or not, feel free to drop me a line, and we can have a no-obligation chat and possibly organise a review.

What does all this mean for the Coventry rental market?

The continued shortage of Coventry rental properties means it will be more difficult than ever to find a Coventry property to rent, and so rents will continue to grow.

Unlike in Scotland, England and Wales do not have rent controls, with Westminster ruling out the possibility of introducing rent control here to deal with the cost-of-living crisis.

You would think rent controls would be a no-brainer, yet economists from around the world have proved for the last 75 years that rent controls might help tenants in the short term, yet ultimately it drives landlords to sell their investments in the long term, thus reducing the stock of available properties to rent out (not great for future tenants).

Therefore, it is highly likely that Coventry rents

will continue to rise for tenants.

Landlords who persevere with their Coventry buy-to-let properties or become a Coventry buy-to-let landlord are set to benefit because they have an asset in very high demand.

The housing shortage, not to mention the other issues discussed above that are affecting the supply of rental properties, is unlikely to be fixed anytime soon!

In conclusion, the Coventry rental market is a constantly changing picture. What is known is that the supply of rental properties is far from what is needed, which can only be to the benefit of buy-to-let investors rather than of tenants renting.

I see buy-to-let as a long-term investment. Everyone reading this knows that the real value in your buy-to-let investment is playing the long game, allowing your Coventry buy-to-let investment to grow over time. Like the crypto or stock market, getting sucked in by get-rich-quick schemes that are selling ‘apparent quick wins’ in property investment is very easy.

I regularly highlight the best buy-to-let deals for Coventry landlords with all the estate agents (not just my own). You don’t need to be a client of mine either to receive that information. Drop me a line or call (without any cost or obligation) if you are interested in making your first Coventry buy-to-let investment or considering adding to your existing Coventry portfolio.

I often get asked what is going to happen to Coventry house prices.

Many things affect house prices, and it comes down to simple supply and demand.

On the supply side of the equation, in the short-term, the number of people wanting to sell their property at any one time has a massive effect on house prices.

In 2007, the number of properties that came onto the market in Coventry jumped drastically. In January 2007, 2,546 properties were available for sale in Coventry and by October in the same year, that had risen to 3,364 properties.

This flooded the Coventry market with houses to buy whilst, at the same time, the banks almost stopped lending money because of the Credit Crunch, thus causing the house price crash of 2008.

Also, on the supply side of the equation is the total number of houses in the whole country (irrespective of whether they are on the market or not). This is an essential factor in house prices, although that has a longer-term effect. Governments can control the number of properties being built with changes in planning regulations, incentives for builders and the buyer schemes such as the Help to Buy plan.

On the demand side of the equation, property values typically rise if homeowners believe they will be wealthier in the future.

Typically, that occurs when the whole country’s economy is performing well as more Brits are in work and salaries are higher. The opposite is also the case when the economy goes into recession; people tighten their spending, lose their jobs, and thus, house prices drop. Inflation will affect British household budgets (because if more of the household budget is going on increased bills, there is less available for mortgage payments).

Another factor on the demand side for housing is when the population increases (through people living longer or increasing net migration) or when the divorce rate increases (making one family household into two single-person households). As always, rising demand typically means higher house prices.

One aspect of the demand side of housing that the Government can control is the taxation of moving home. In the late spring of 2020, the Government vastly reduced the tax (Stamp Duty) paid to buy a house, saving many home buyers thousands of pounds.

Also, on the demand side, property values usually increase if more homebuyers can borrow more money with a mortgage to buy their home.

The more banks and building societies can offer mortgages, the more homebuyers can buy their future home, thus raising house prices.

However, the constraint is the amount a home buyer can borrow on a mortgage.

What someone can borrow depends on what they earn and if they can afford the monthly mortgage payments. The level of mortgage payments is dependent on three things.

How much you borrow

The interest rate charged

The length of the mortgage

The lower the interest rates are, the lower the cost of borrowing to pay for your house is and thus more people can afford to borrow money with a mortgage to buy a home, meaning house prices tend to go up.

Coventry house prices have risen by 84.16% between 2010

and today, mainly fuelled by low interest rates.

So, looking at everything above, apart from Stamp Duty and the incentives for buyers (which historically have made a minimal difference), the Government in the short-term, irrespective of who the Prime Minister is, makes little difference directly to house prices.

The most significant short-term factor which directly

affects house prices is interest rates.

However, the Bank of England (not the Government) sets the interest rate for the UK economy. That means the Government (and Rishi as PM) cannot directly make any differences in house prices (apart from the points raised above).

Yet, indirectly, as seen with the Liz Truss/Kwasi Kwarteng Mini-Budget catastrophe only a few weeks ago, what the Prime Minister (and their Government) does can make a massive difference to interest rates and, thus, the property market and house prices.

Since December 2021, the Bank of England has been slowly raising interest rates to combat inflation. Unfortunately, the downside is that it increases the mortgage rates homebuyers must pay if they are on a variable-rate mortgage or coming off a fixed-rate deal secured a few years ago.

As 17 out of 20 homebuyers have a fixed-rate mortgage, when a bank or building society calculates a 5 or 10-year fixed-rate deal, they consider what the Bank of England interest rate is today, but they also consider something equally important, something called the ‘swap rate’.

As Coventry homeowners and landlords, it is vital you should be aware of the swap rates as they are based on what the global money markets think future UK interest rates will be.

If the swap rate rises, then mortgage lenders will increase their rates on the mortgages they offer, and by doing so, (as discussed previously in this article), increased mortgage rates will affect affordability and, thus, house prices.

So, what affects UK swap rates? Mainly one thing, the price of government debt in the form of gilt yields

Given the vast increase of planned government debt originally announced in that mini-budget by Truss/Kwarteng, the money markets who would be lending the Government the billions of pounds to fund those tax cuts got worried the Government wouldn’t be able to pay back such a rise in borrowing, so wanted a higher rate of return on the money they were lending the Government.

That return is measured in the ‘gilt yield rate’, and the gilt yield rate directly drives the ‘swap rate.’

That rise in the gilt yield rate/swap rate was the main reason mortgage rates rocketed after the mini-budget and helped in the collapse of Liz Truss’s Prime Ministership.

So, what can Coventry homeowners expect in the coming weeks and months with gilt/swap rates?

Rishi Sunak’s first job was to re-establish confidence in the money markets for UK plc. During the summer, the 5-year gilt rate rose steadily from 1.6% to 3.5%, in line with the general rise in Bank of England base rates. Yet when the mini-budget was delivered on the 23rd of September 2022, that rose almost straight away to 4.6%.

That meant every mortgage rate jumped in price by

1 to 1.5% almost overnight.

At the time of writing, the 5-year British gilt yield has dropped to 3.5%, and the others have either dropped below their pre-mini-budget rate or were moving in that direction, depending on the gilt type.

The gilt rate (which directly affects the swap rate, which in turn, directly affects mortgage interest rates) could drop further, subject to what Rishi Sunak and his Chancellor Jeremy Hunt have planned in the Budget (and supplementary report from the Office for Budget Responsibility) on the 17th of November 2022.

A drop in the gilt/swap rate is vital for any Coventry homebuyer buying a house or Coventry homeowner re-mortgaging to a new mortgage deal. Why? Because …

with the average Coventry home worth £242,731 (a rise of 7.89% over the past year), each 1% extra in the mortgage rate would cost every Coventry homeowner an additional £202.28 per month.

So, what does this all mean for Coventry house prices, then?

Greater certainty will keep the volume of housing transactions ticking over, yet not inescapably Coventry house prices.

In my blog articles on the Coventry property market, I believe Coventry house prices will be lower in 12 months, and I expect Coventry prices to return to where they were in the late spring/early summer of 2021.

And why is that? Unlike the 2008 Credit Crunch house price crash, today, the country has very low levels of unemployment and very well-capitalised banks (because the Bank of England subsequently forced them to keep lots of cash in their banks to cover downturns). Therefore, I don’t anticipate the kind of double-digit house price decreases seen 14 years ago.

If you would like to pick my brain about the Coventry property market, be you a potential Coventry first-time buyer, a Coventry homeowner looking at your options on re-mortgaging or selling, or, in fact, anyone with questions, don’t hesitate to drop me a line. I will gladly share my thoughts and opinions without cost or obligation.

Most Coventry homeowners born before 1960 have been in their homes for more than 25 years.

Yet of all the properties sold in the UK since the first lockdown in the summer of 2020, 50% of those property owners had only been in their homes for six years and four months or less. That means we almost have a two speed housing market.

One market of homeowners in their 20s and 30s who move every four to five years and another property market of homeowners who, when they hit their late 40s, tend to stay put for decades. Yet now those mature homeowners, many of whom are retired and on fixed incomes with pensions, are finding it a lot more challenging to make ends meet with the cost-of-living crisis.

Evidence suggests nationally and locally, a lot of larger houses (property which tends to be owned by mature homeowners) have come onto the market in the last 12 months compared to the previous few years.

There has been a drop of 22.9% of properties priced up to £200,000 on the market in the UK in the last 12 months, yet an increase of 13.3% of properties priced between £500k and £1m. Focusing on the lower price range nationally, there are 39.4% fewer properties for sale in the price range up to £100k, 27% fewer in the £100k to £150k range and 14.9% fewer in the £150k to £200k range. The range that has seen the highest growth is the £600k to £750k, which has grown by 14.2%.

Looking closer to home in Coventry…

there are 20% more properties for sale in the Coventry area today compared to a year ago.

(1,317 properties for sale now compared to 1,102 a year ago).

But it gets much more interesting when you split the increases by bedrooms and property type.

Properties with more bedrooms tend to be more expensive than those with fewer. Also, detached and semi-detached properties are more expensive than terraced/townhouses and apartments.

5-bed Coventry properties – an increase of 27%

4-bed Coventry properties – an increase of 14%

3-bed Coventry properties – an increase of 39%

2-bed Coventry properties – an increase of 8%

1-bed Coventry properties – a decrease of 27%

And now, by type…

Coventry detached properties – an increase of 24%

Coventry semi-detached properties – an increase of 51%

Coventry terraced/town house properties – an increase of 45%

Coventry apartments – a decrease of 25%

The increase in these larger Coventry homes is great news for second or third-time movers, as it releases larger homes for them to bring up their young families.

Yet, the other side is the lack of properties for these mature Coventry homeowners to buy.

There are 12.7 million people aged 65 and over in the UK (19% of the total population), yet there are only 2 million bungalows (which represent 7.2% of all UK property).

When it comes to new properties, the figures are even worse.

Of the 173,660 properties built in 2019, only 2,384 were bungalows.

And this is where the annexe could be one part of the solution.

Annexes are buildings often erected in gardens or extended onto an existing property to be used as separate and independent living accommodation.

Generally, the ‘granny annexe’ has been used to keep one’s parents and grandparents nearby whilst retaining their independence. Roll the clock back to the Millennium, annexes were seen as excess accommodation that added little to the saleability or value of property.

Interestingly though, in the last few years, the annexe has had a renaissance and has become a practical, economical and emotional answer for a more flexible group of homeowners.

Lockdown brought working from home to the fore, and the annexe is undoubtedly an excellent solution for many homeowners.

Lockdown saw many people recognise the importance of having their family close by. I have seen several mature Coventry homeowners build an annexe extension in the garden, then move into the annexe themselves and give their original property to their children to live in. Thus helping two families with their accommodation needs and the advantage of shared fuel costs (plus other benefits such as childcare).

Also, as mortgage rates are rising, the annexe could be the salvation for either your first-time buyer child/grandchild who cannot afford to buy their first home because of mortgage affordability rules or who is finding it tough to save a deposit for a mortgage.

The demand is there for annexes. In December 2020, Rightmove reported a year-on-year 89% increase in the number of home buyers and tenants searching for the term ‘annexe’. Demand is high and supply, as seen by these statistics, is low.

Of the 1,317 properties for sale in the Coventry area, only 14 have an annexe.

I believe the lockdown made many of us look at how we live in the UK. Many people are adopting, adapting and changing how they look at housing. With recent planning regulation changes, the rules were relaxed a few years ago, which allowed homeowners to extend their homes without planning permission in an arrangement called ‘Permitted Development’.

If you are a mature/older Coventry homeowner or have mature/older parents and want to look at all your options regarding upsizing, downsizing and annexes, then without any obligation, drop me a message and let’s chat through your options.

For everyone else in Coventry, what do you think about annexes? And what other solutions could help solve the housing issue in Coventry and the UK as a whole?

What an amazing week that has been in the property market!

The new government has decided to redesign the wheel and completely change the economic policy of the Boris Johnson government. Whatever your political point of view, the actions taken clearly haven’t gone down well with the markets and seem to fly in the face of the priorities of the Bank of England.

The turmoil created has left many homebuyers and owners wondering what the future may hold for mortgage rates and payments, especially those that are hoping to buy in the next 1-2 years or whose fixed rate deals are coming to an end during that same period.

Kenilworth may perhaps be less vulnerable to the potential issues, with an older population and probably a higher percentage of property owners who are mortgage free or with much lower loan to value borrowing. However there are still a proportion of first time buyers in Kenilworth, there are also a volume of rental properties which will be mortgaged on buy to let deals.

And what will happen to prices through all of this? The million dollar question. The cost of home ownership is set to increase, so demand may be dampened to a certain extent whilst rents will also increase as landlords pass on the additional costs to their tenants. However, there is still a shortage of supply as the number of new homes being built continues to fall short of the targets set, so it is unlikely that prices will fall much, if at all, though they will probably fall in real terms as inflation outstrips any price increases over the next few months.

If you are buying then now could be a good time to find bargains so keep your eye on the market for motivated sales and deals to be had. Shrewd buyers will realise that the next few months could be a fantastic time to purchase before the market recovers and heads north again as it inevitably will.

If a buyer has one particular objection about a property then this is often a positive sign. So if they are worried about the busy road but like the property generally then it’s the job of your Estate Agent to sell them the positives and try to persuade them to make a compromise on this particular point, perhaps by mentioning that similar properties on a quieter road would cost that much more. Or maybe if the garden isn’t quite as big as they hoped, the generous living space will make up for this and again, the buyer may be prepared to compromise.

If a buyer has one particular objection about a property then this is often a positive sign. So if they are worried about the busy road but like the property generally then it’s the job of your Estate Agent to sell them the positives and try to persuade them to make a compromise on this particular point, perhaps by mentioning that similar properties on a quieter road would cost that much more. Or maybe if the garden isn’t quite as big as they hoped, the generous living space will make up for this and again, the buyer may be prepared to compromise.